Here is news from several states. I don’t think most states will strive to collect below the thresholds of the South Dakota law, but you never know. I think we’ll hear from more states by early 2019 and perhaps even from a few members of Congress. I’ll continue to update this post.

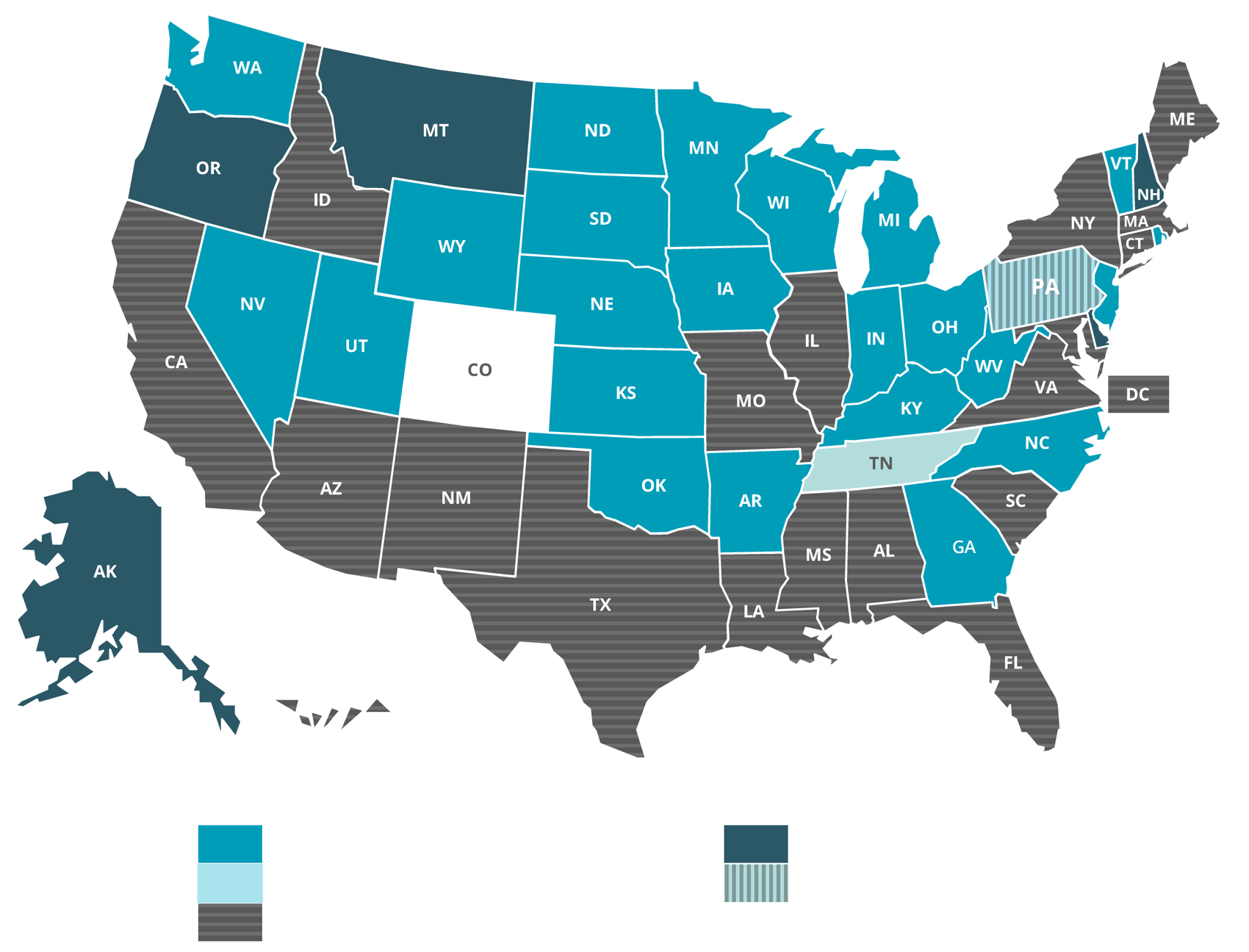

States in bold are full members of the Streamlined Sales and Use Tax project. The SSUTA scheduled an emergency meeting of the SSUTA Board for July 19-20 to discuss the Wayfair decision. Agenda items included use of the Central Registration System and the Certified Service Provider system by non-members.

Also look for what applies for local governments, particularly in Alabama, California (see below), Colorado, and Louisiana.

Also, on 6/29/18, the National Conference of State Legislatures released its Principles of State Implementation after South Dakota v. Wayfair. This 1-page document suggests that states be prepared before more broadly enforcing tax collection and wait until 1/1/19 to start collecting. It also includes suggestions for states that that have not adopted the Streamlined Sales and Use Tax Agreement (SSUTA).

-

- Alabama – The Dept. of Revenue released a statement on 7/3/18 that reminds readers that the DOR issued economic nexus sales tax rules in 2016. Per the DOR, these will be applied prospectively starting for sales made after 9/30/18, even though the rules were effective 1/1/16. The threshold for economic nexus under the rules is annual sales in the state above $250,000, The statement also notes the state’s marketplace facilitators law also for sales exceeding $250,000. These facilitators must collect sales tax on sales of its third-party sellers or comply with the reporting and customer notification rules. Also see HB 470 enacted in April 2018 extending collection to marketplace facilitators and Reg 810-6-2-.90.03.

- Arkansas – SB 576 (Act No. 822; 4/10/19) – imposes marketplace facilitator collection obligations if deliveries to state exceed $100,000 or 200 transactions.DOR FAQs for Remote Sellers.

- California – This is one of the states that already had broad language in its statute that with the repeal of Quill, likely allows the state agency (California Department of Tax and Fee Administration (CDTFA)) to start collecting from remote vendors with over $100,000 of sales in the state or 200 or more transactions. I say “likely” because while California Revenue & Taxation Code Section 6203(c) provides that retailer in the state includes “any retailer that has substantial nexus with this state for purposes of the commerce clause of the U.S. Constitution,” is the $100,000 receipts or 200 transaction threshold enough for the state? The U.S. Supreme Court noted three aspects of the SD law that supported nexus within commerce clause parameters (see page 23 of the opinion): (1) safe harbors of the $100,000 receipts or 200 transactions, (2) no retroactive application, and (3) SD belongs to the SSUTA which requires states to offer free software for compliance and audit protection if used, as well as standardized definitions and other administrative benefits. While the CDTFA can offer (1) and (2), it can’t easily offer (3). That would likely take some additional appropriations. In fact, given the size of California, its customer base likely supports many remote vendors who meet the safe harbors of the SD law. Can the CDTFA handle all of the new registrations and support that would be needed without an allocation of more funds? Also, might the legislature of this state that is home to eBay, want to raise the safe harbor thresholds? And, how important is (3)? Are factors (1) and (2) enough?Hearings: On 10/15/18, the Senate and Assembly taxation committees held a joint information hearing. On 10/24/18, the CDTFA held an informational hearing on Wayfair.CDTFA Action: On 12/11/18, the CDTFA announced that it would follow the SD thresholds as measured in the prior or current calendar year, starting 4/1/19 (Special Notice L-565 (Dec. 2018)). Also, in-state sellers must apply the Wayfair standards to determine if they must collect district taxes anywhere they ship in California and are not already collecting in that district (such as because they don’t have a physical presence there) (Special Notice L-591 (Dec. 2018)). Also see CDTFA website and FAQs – here.AB 147 Enacted (Chapter 5, 4/25/19) – this makes significant changes to the CDTFA action including that the transaction quantity standard is removed, the sales threshold is increased to $500,000, a marketplace facilitator collection requirement is added (starting 10/1/19) and a vendor with over $500,000 of sales will also have to collect the district level tax (the local tax beyond the state rate of 7.25%) regardless of the amount of sales in a district. The new thresholds apply starting 4/1/19. Also see CDTFA Notice L632. Also see CDTFA proposed amendment to Reg 1684 for the new changes.

- Colorado – See new website links here. Tax collection for remote sellers starts 12/1/18. Sellers meeting the new nexus thresholds are to register by 11/30/18. The thresholds are the same as for South Dakota

- Connecticut – SB 417 (Public Act 18-152; 6/14/18) modifies the states economic nexus for sales tax for remote vendors to having at least $250,000 of retail sales in the state and 200 or more transactions, effective 12/1/18. Also see Dept. of Revenue Services Special Motice (5.1) explanation of the law change related to Wayfair, as well as the explanation of the marketplace facilitator law change.

- District of Columbia (DC) – B22-0914 (Act No. A22-0584; 1/18/19) adopts the SD thresholds. The revenues generates are to be used to lower commercial property tax rates. Also see DC’s Office of Tax and Revenue website on sales tax.

- Georgia – At 1/1/19, follows an economic nexus standard of over $250,000 of sales into the state in the prior or current calendar year or 200 or more separate retail sales of tangible personal property. Alternatively, the vendor must issue a notice to the buyer and state. See HB 61 (Act 365, 5/3/18). Click here for more information from the Georgia Dept. of Revenue.

- Hawaii – Prior to the Court’s decision, Hawaii enacted SB 2514(Act 41, 6/13/18) to match the SD law, effective 7/1/18, but applying to tax years beginning after 12/31/17. In Announcement No. 2018-10 (6/27/18), the Dept. of Taxation stated that it had been unclear when its general excise tax (GET) applied when a seller did not have a physical presence in the state. Act 41 though, provides clarification. Starting 7/1/18, taxpayers must obtain a GET license and file returns and remit the GET if for the current or prior year the taxpayer had gross income or proceeds of $100,000 or more, or 200 or more separate transactions from tangible property delivered in Hawaii, services used or consumed in Hawaii or intangible property used in Hawaii. Thus, Hawaii started with an effective date (retroactive) of 1/1/18 (that is, a vendor could have crossed the requisite threshold in 2017 making it subject to collection starting 2018). However, on 7/10/18, the Dept.of Taxation announced that because the Supreme Court noted that SD law was not retroactive, to avoid constitutional challenge, Hawaii will not apply its law to sellers who lacked physical presence prior to 7/1/18 (see amended announcement).

- Idaho – The State Tax Commission issued an explanation on 8/15/18. Remote retailers must collect if they have an agreement with an Idaho retailer to refer buyers to the remote seller for a commission on the sale, and total sales to in-state buyers due to such agreements exceeds $10,000 in the prior 12 months. This is the state’s “click through” nexus rule. The announcement states that the Tax Commission is “carefully analyzing” how the Wayfair decision affects remote sellers.HB 259 (enacted 4/9/19; Chapter 320), effective 6/1/19 – internet retailers and marketplace facilitators to collect and remit sales and use tax. See summary in summer newsletter of the State Tax Commission..State Tax Commission’s guide for online sellers.

- Illinois – Enacted HB 3342 (Public Act 100-0587)on 6/4/18. Article 80 includes a “marketplace fairness” provision providing that a vendor is considered a “retailer maintaining a place of business” in the state if it makes sales of tangible personal property to buyers in the state, from outside of the state and have cumulative gross receipts from sales of such property of $100,000 or more, or has 200 or more separate transactions for the sale of tangible personal property to Illinois buyers. The determination is made quarterly by looking 12 months back from the last day of March, June, September or December. If the criteria is met, the retailer must collect and remit sales tax for one year. At the end of that year, if the criteria continue to be met, collection continues. Effective starting 10/1/18.

- Indiana – Has an amnesty program through the end of 2018 for online vendors who should have been collecting such as because they have inventory in the state. The DOR released a statement noting that on 6/21/18, Governor Holcomb said they were studying ruhe ruling “to better understand its implications for Indiana.”

- Iowa – Prior to the Court’s decision, Iowa enacted SF 2417effective 1/1/19 which basically mirrors South Dakota law. On 6/25/18, the Dept. of Revenue issued an explanation and a reminder that if a vendor has physical presence and has not been reporting, it should consider the voluntary disclosure purposes. The new economic nexus law is prospective only (starting 1/1/19) including the requirement that marketplace facilitators meeting the SD threshold collect starting 1/1/19. For an example of how the expanded sales tax nexus can apply to a remote vendor, see the DOR’s ruling in Fairytale Brownies, Inc., an Arizona-based company selling product into Iowa (Dkt No. 2018-300-2-0440; 12/7/18). The company’s website indicates it collects tax on sales to Iowa customers starting 1/1/19.H 779 (5/16/19) – removes the 200 transaction threshold.

- Kentucky – DOR news release on HB 487, which would adopt the South Dakota thresholds, effective 7/1/18.

- Louisiana – The Department of Revenue issued a statement on 6/21/18 that “it is far too soon for a definitive estimate of what the state will receive from online sales as a result of today’s decision, but when appropriate, we will provide updates.” Update: On 8/10/18, the DOR issued Remote Sellers Information Bulletin No. 18-001 on the impact of the decision. Legislation in 2017 created the Louisiana Sales and Use Tax Commission for Remote Sellers. The Commission will not seek to enforce collection on remote sellers for any period beginning before 1/1/19. The Bulletin also observes “there is no requirement in the Wayfair decision that states adopt the Streamlined Sales and Use Tax Agreement in order to meet Commerce Clause standards.” Additional guidance will be released “as appropriate.”DOR’s Remote Sellers Information Bulletin No. 19-001 (5/17/19).Observation: The Supreme Court did note three features of SD law “that appear designed to prevent discrimination against or undue burdens upon interstate commerce.” One of these features is that SD is a member of the SSUTA meaning it has some uniform definitions as well as provides software to vendors and audit protection if it is used. [case page 23]

- Maine – A 2017 law change (36 M.R.S. §1951-B(3); Chapter 245) adopted the SD thresholds. In a 10/1/17 newsletter, the Department of Revenue says the change is effective 11/1/17, but the legislation says effective once permitted per the U.S. Constitution. Also see tax agency’s August 2018 release and website.

- Maryland – A undated Tax Alert from the Comptroller states reminds folks that Maryland law imposes sales tax collection obligations “as broadly as is permitted under the United States Constitution. It includes an interesting “figure it out yourself” statement: “If you sell or deliver tangible personal property or a taxable service for use in Maryland, you should review and analyze the United States Supreme Court’s decision in [Wayfair] to identify how it affects you.”In September, the state got more specific noting it would follow the South Dakota approach starting 10/1/18.

- Massachusetts – in a 6/22/18 news release, the Department of Revenue noted that its existing regulation 830 CMR 64H.1.7(Vendors Making Internet Sales), effective October 2017 remains in effect and is not affected by the Wayfair decision. This regulation has also been referred to as the “cookie nexus” rule. This regulation includes the following:

“Unlike the mail order vendor at issue in Quill, Internet vendors with a large volume of Massachusetts sales invariably have one or more of the following contacts with the state that function to facilitate or enhance such in-state sales and constitute the requisite in-state physical presence. …”

- property interests in and/or the use of in-state software (e.g.,“apps”) and ancillary data (e.g.,“cookies”) which are distributed to or stored on the computers or other physical communications devices of a vendor’s in-state customers, and may enable the vendor’s use of such physical devices;

- contracts and/or other relationships with content distribution networks resulting in the use of in-state servers and other computer hardware and/or the receipt of server or hardware-related in-state services; and/or

- contracts and/or other relationships with online marketplace facilitators and/or delivery companies resulting in in-state services, including, but not limited to, payment processing and order fulfillment, order management, return processing or otherwise assisting with returns and exchanges, the preparation of sales reports or other analytics and consumer access to customer service.”The sales tax collection thresholds is over $500,000 of sales into the state AND 100 or more transactions in the prior calendar year. Also see the state’sFAQs.

-

- Michigan – Per Revenue Administrative Bulletin 2018-16(8/1/18), starting 10/1/18, remote sellers with both taxable and non-taxable sales into the state in excess of $100,000 or 200 or more separate transactions based on the prior calendar year, has nexus and must register and start collecting. No tax is owed prior to this date (unless they otherwise had nexus such as under the state’s click-through nexus rule). If sales level later drop for a calendar year, the seller can stop collecting the next year. Also see FAQs on remote sales in light of the Wayfair decision.

- Minnesota – The Department of Revenue issued a news release on 6/21 stating that the Wayfair decision means that “states like Minnesota can require certain retailers with no physical presence, such as online sellers, to collect and remit the applicable sales or use tax on sales delivered to locations within their state.” The DOR also stated that they “will work with our customers to ensure fair, efficient, and transparent implementation of this decision. We will provide further guidance within 30 days. The department will work hard to provide our customers with the information and services they need to meet their sales and use tax obligations under Minnesota tax law in as smooth and efficient manner as possible.” The DOR expects to issue guidance within 30 days for vendors not presently collected sales tax from Minnesota customers. The DOR also observes that vendors who want to start collecting now can register to do so with Minnesota and the other 23 member states of the Streamlined Sales Tax System at https://www.sstregister.org/.In a 7/17 memo, the DOR noted it is hosting the emergency meeting of the SST Governing Board on July 19 and 20. Also, an announcement about sales tax enforcement for remote sellers and marketplace providers will by made on 7/25/18. The DOR also has a “red envelope” on its website where remote sellers can sign up to get emailed updates.A 7/25 memo from DOR states that remote sellers and Marketplace Providers that facilitate sales will be required to start collecting sales tax by 10/1/18. This memo includes links to the relevant law (297A.66) and some FAQs for remote sellers. Small remote sellers are exempt from collection if during the prior consecutive 12-month period they had less than 100 retail sales shipped to Minnesota and less than ten retail sales shipped to Minnesota that total over $100,000.

- Mississippi – The Department of Revenue stated in a 6/21/18 release that it is studying the Wayfair ruling to determine its effect in the state. “It is our belief this will create a more level playing field for Mississippi businesses that compete with online sellers.” The DOR reminds sellers with out a physical presence in the state that existing state law requires those with sales in excess of $250,000 in the prior 12-month period to register and collect sales tax. Also see DOR “Sales and Use Tax Guidance for Online Sellers” updated for the Wayfair decision.

- Montana – Has a website explaining the effect of Wayfair on its residents and in-state businesses. Montana does not itself impose a sales tax. They suggest that in-state vendors “seek competent legal advice on how to proceed with collecting and remitting sales tax for sales tax states such as South Dakota.”

- Nebraska – On 7/27/18, the DOR issued a news release with reminders to consumers to pay use tax when not charged sales tax, to certain remote sellers to check state law (Neb. Rev. Stat. 77-2701-13) to see if they must register to collect sales tax, and to in-state sellers that they may have new collection obligations in other states. State law includes affiliate ownership, and various in-state connections. It also includes that engaged in business includes soliciting orders in a “continuous, regular, seasonal, or systematic” manner where the “retailer benefits from any banking, financing, debt collection, or marketing activities occurring in this state or benefits from the location in this state of authorized installation, servicing, or repair facilities.” Also see the DOR FAQs on the Wayfair decision. So, watch for any action by the legislature to adopt South Dakota-type legislation.LB 284 (signed 3/21/19) uses the SD thresholds and adds marketplace facilitator collection requirements. See text.

- Nevada – The Nevada Tax Commission released a draft regulation on 7/17/18 (R189-18) that basically adopts the SD threshold for a remote vendor to be subject to sales tax obligations in the state. A revision was released 8/9/18. See actions and timeline posted here.

- New Hampshire – Governor Sununu news release of 6/28/18 to fight the decision. Another press release of 8/23/18 lists executive actions underway including helping in-state businesses avoid scams where a thief posing as a state collector tries to get money or sensitive customer data from them. NH doesn’t impose a sales tax.On 7/19/19, Governor Sununu signed SB 242 (Chapter 280) presenting an approach to try to fight other states imposing collection duties on NH sellers. The summary of this legislation states that it provides “for protection of private customer information and rights of New Hampshire remote sellers in connection with certain foreign sales and use taxes.” SB 242provides that other states must first provide notice to the NH Dept. of Justice before requesting private customer information, performing exams, or imposing sales and use tax collection obligations on NH sellers. A commission is established to monitor federal and state law changes and proposals regarding tax collection obligations on NH remote sellers. Section 2 of SB 242 takes effect 11/1/20 and the rest takes effect on 7/19/19. It is not clear from the text what “Section 2” is. See Governor Sununu news release on signing SB 242.

- New Jersey – legislation is pending. Also, on 8/14/18, the NJ Division of Taxation issued a notice that effective 10/1/18, consistent with the Wayfair decision, remote vendors meeting the SD thresholds in NJ must register and collect sales tax. FAQs.

- New York – Per the Dept. of Taxation and Finance website, a vendor is subject to sales tax collection if in the immediately preceding four sales tax quarters, their cumulative total gross receipts from sales of tangible personal property delivered into NY exceeded $300,000, AND the vendor made over 100 sale of tangible personal property delivered into NY. Also see N-19-1(Jan. 2019) on sales tax registration for businesses without a physical presence in the state.S01509C and A02009-C (signed 4/12/19; Chapter 59) – adds marketplace provider collection requirement.

- North Carolina – Sales and Use Tax Directive 18-6 (8/7/18) – The DOR will apply the Wayfair decision prospectively starting 11/1/18. By “Court’s ruling in the Wayfair decision,” the DOR means application of collection obligations to remote sellers with gross sales exceeding $100,000 or 200 or more separate transactions in the prior or current calendar year. Such sellers must register 11/1/18 or 60 days after they meet the threshold, whichever is later.SB 56 (signed 3/20/19) adopts the DOR thresholds.

- North Dakota – The Tax Commissioner states that remote sellers must now follow ND’s law enacted in 2017 (SB 2298; 4/10/17) that is similar to that of South Dakota. At 6/25/18, the website states that it is a “work-in-progress” and more information will be added later.

- SB 2298 included a “contingent effective date” provision: “This Act becomes effective on the date the United States Supreme Court issues an opinion overturning Quill v. North Dakota, 504 U.S. 298 (1992), or otherwise confirming a state may constitutionally impose its sales or use tax upon an out-of-state seller in circumstances similar to those specified in section 1 of this Act.”

- SB 2191 enacted 3/14/19 removes the 200 transaction requirement effective for tax years beginning after 2018.

- SB 2338 enacted 3/27/19 imposes collection obligations on marketplace facilitators effective 10/1/19.

- Ohio – Dept. of Taxation memo on Substantial Nexus and Marketplace Facilitator Changes in light of HB 166 taking effect 8/1/19.

- Oklahoma – The State Treasurer’s June/July 2018 Economic Report includes an overview of the Wayfair case. It also reminds readers that the effect of the decision is “not a tax increase, but a tax compliance issue.” It also notes the benefit to cities, estimated at about $112 million annually.

- Pennsylvania – Sales and Use Tax Bulletin 2019-01 (7/1/19) – Maintaining a Place of Business in the Commonwealth – basically, the state uses the $100,000 gross sales threshold and explains how that level applies for marketplace facilitators and marketplace sellers. Also see the DOR’s sales tax, economic nexus and Wayfair website + information on marketplace facilitator rules.

- Rhode Island – The Dept. of Revenue issued an advisory on 6/27/18 to remind remote vendors of registration options. RI is a member of the Streamlined Sales and Use Tax System. The advisory doesn’t state though which vendors need to register. Also see DOR Pub 2018-06 (7/6/18) with FAQs for remote sellers. DOR ADV 2018-29 (7/23/18) provides additional information for non-collecting retailers.

- South Carolina – On 8/10/18, the DOR released three draft rulings. Draft SC Revenue Ruling #18-x, Retailers Without a Physical Presence (“Remote Sellers”) – Economic Nexus, effective for sales made on or after 10/1/18, sellers meeting a $250,000 economic nexus standard must register and collect sales tax. Draft SC Revenue Ruling #18-x, Online Marketplaces – Physical and Economic Nexus, provides information for marketplaces and sellers using them as well as the relevance of the litigation involving Amazon. The third ruling, Draft SC Revenue Ruling #18-x, Persons Using Another Person’s Online Marketplace To Sell Their Products – Registration and Tax Collection Guidance. On 8/21/18, another draft ruling was released: Draft SC Revenue Ruling #18-x, Local Sales and Use Taxes and Catawba Tribal Sales and Use Tax.

- South Dakota – On 10/31/18, Governor Daugaard and Attorney General Jackley announced a settlement with Wayfair, Overstock.com and Newegg where these companies would start collecting sales tax on 1/1/19. Other remote vendors subject to the SD law were required to start collecting 11/1/19! See the Dept. of Revenue’s website about the state’s famous economic nexus law.Information on remote sellers and marketplace providers + FAQs.

- Tennessee – Sales and Use Tax Notice #18-11 (August 2018) states that its economic nexus rule is not enforceable until the General Assembly reviews the Wayfair decision. “However, the Department encourages these dealers to voluntarily collect and remit the tax as a convenience to their customers.” The notice states that the economic nexus rule (Rule 129(2)) will not be applied retroactively.

- Texas – Comptroller Hegar announced 6/27/18 his office would study the situation with input from the public and lawmakers. He suggested there would be no retroactive application. STAR ruling 201807004L (7/5/18) summarizes the Wayfair decision, notes what the Comptroller is doing, and offer suggestions for the stat legislature. On 10/19/18, proposed rules were issued (see page 24, et seq). A threshold of over $500,000 of sales in a year is proposed and no transaction test. Also, once the seller crosses the threshold, it has three months before starting to collect. Vendors who cross the threshold now, start collecting 10/1/19.In November 2018, SB 70 was introduced calling for a single statewide local tax rate for remote vendors.See more news in the December 2018 Comptroller’s newsletter.

See Comptroller’s website on Wayfair for sellers. - Utah – SB 2001 enacted after the Court’s decision in Wayfair, follows the South Dakota thresholds, effective for sales on or after 1/1/19. This new law repeals the 18% discount Utah had been offering to remote sellers who voluntarily collected the state’s sales tax.

- Vermont – The Dept. of Taxes announced that the Court’s decision makes Act 134 (2016) effective. That law is similar to that of SD affecting out-of-state vendors that made at least $100,000 or sales or 200 individual transactions in any prior 12-month period.

- Virginia – HB 1722 (Chapter 815; 3/26/19), effective 7/1/19 imposes the over $100,000 gross revenue or 200 or more separate retail sales transactions threshold, as well as marketplace facilitator collection obligations. SB1083 (Chapter 816; 3/26/19) effective 7/1/19 is similar and discusses liability relief for facilitator if collects wrong amount of tax.Guidelines for Remote Sellers and Marketplace Facilitators from DOT, effective 6/27/19.

- Washington – The DOR website notes that starting 10/1/18, the South Dakota threshold will apply. If the remote seller only sells through a marketplace facilitator, different rules apply. In addition, starting 1/1/18, remote sellers and marketplace facilitators with $10,000 or more in retail sales in-state must either register their business and collect sales tax or follow the use tax notice and reporting requirements. However, it cautions that any business meeting the SD thresholds must start collecting (and register) starting 10/1/18.SSB 5581 signed 3/14/19 removes the 200 transaction and just uses the over 4100,000 of sales for nexus.

- Wisconsin – The DOR website states that starting 10/1/18, remote vendors will have to start collecting sales tax from Wisconsin customers if they meet the new standards that match the SD thresholds. The website also has a set of FAQs. Also see DOR’s Statement of Scope regarding work needed. The Legislative Fiscal Bureau reports in a 7/2/18 memo that if the state changed its law to follow SD law, it would generate an additional $120 million per year. It also notes that state law likely needs to be changed to specify a threshold for “an electronic nexus threshold.” The memo also notes that a law change in 2013 states that additional sales and use tax revenues generated from “any federal law” expanding the ability of the state to impose sales tax obligations on remote vendors is to be used to reduce income tax rates.

-

- Wyoming – The DOR issued a memo reminding readers that the state has an economic nexus rule similar to that of SD. The DOR is studying the decision’s “impacts” to determine a “date certain for licensing deadline.” The rule will be enforced prospectively only.

States with South Dakota type laws will need to issue guidance on the effective date and how to measure the $100,000 sales and 200 transaction thresholds (or other thresholds specified by the state). For example, do sales of tax-exempt items count?

Have you checked the existing sales tax nexus/jurisdiction law in states where you or clients have nexus per the South Dakota standard? As standards differ among states, some states have not yet said anything about their response to the Wayfair decision, and after the decision, e-commerce vendors are more likely to have new sales tax obligations. Such vendors should consider a system that enables them to track the number of transactions in each state and the dollar amount to better identify when new collection obligations arise or to consider not making certain sales if they want to reduce the number of states in which they have collection and filing obligations.

What do you think? Annette Nellen

Annette Nellen, CPA, Esq., is a professor in and director of San Jose State University’s graduate tax program (MST), teaching courses in tax research, accounting methods, property transactions, state taxation, employment tax, ethics, tax policy, tax reform, and high technology tax issues.

Annette is the immediate past chair of the AICPA Individual Taxation Technical Resource Panel and a current member of the Executive Committee of the Tax Section of the California Bar. Annette is a regular contributor to the AICPA Tax Insider and Corporate Taxation Insider e-newsletters. She is the author of BNA Portfolio #533, Amortization of Intangibles.

Annette has testified before the House Ways & Means Committee, Senate Finance Committee, California Assembly Revenue & Taxation Committee, and tax reform commissions and committees on various aspects of federal and state tax reform.

Prior to joining SJSU, Annette was with Ernst & Young and the IRS.

{kind=link}

Recent Comments